Today, most crypto neobanks are drifting into a false choice.

Either they replicate the surveillance heavy compliance model of traditional banks. Or they embrace radical opacity and hope regulators tolerate the experiment.

Neither path leads to mass adoption.

If crypto neobanks want to become default financial accounts rather than speculative side products, they must achieve privacy and compliance parity with traditional finance. Not less compliance. Not weaker controls. The same regulatory confidence delivered through a fundamentally different architecture.

What Privacy and Compliance Parity Really Means

Let us make this concrete.

Privacy and compliance parity does not mean avoiding AML requirements or weakening KYC standards. It means achieving the same regulatory outcomes expected from digital banks while offering stronger data protection for users.

In practice, this means:

- Satisfying AML, KYC, sanctions screening, and regulatory reporting standards.

- Providing auditability and enforceable risk controls.

- Giving users meaningful control over their identity data.

Regulators should see familiar guardrails. Risk teams should see enforceable policies. Banking partners should see credible compliance infrastructure.

What changes is not the outcome, but the architecture behind it.

Instead of every crypto platform storing raw passport scans and biometric data, identity becomes a verifiable and privacy preserving layer. This is the foundation of compliant DeFi and the next generation of crypto neobanks.

Why Web2‑style KYC breaks crypto neobanks

To understand why a new model is necessary, we have to examine the limitations of the current Web2 KYC stack.

Traditional KYC systems were designed for closed banking environments operating within single jurisdictions. They were not built for permissionless blockchains, cross chain ecosystems, or global crypto wallets.

As a result, every time a user interacts with a new crypto exchange, wallet, or neobank:

- They repeat the same onboarding process.

- They upload the same documents.

- Their personal data is stored in yet another centralized database.

This creates multiple identity silos across Web3.

- For users, it means friction and elevated data breach risk.

- For builders, it destroys composability.

- For regulators, it fragments oversight across disconnected entities.

In other words, we end up with permissionless financial rails but fully permissioned and duplicated onboarding. Rebuilding Web2 KYC inside crypto neobank does not solve the problem. It amplifies it.

Zero Knowledge Identity: From Data Exposure to Attribute Proofs

This is where zero knowledge identity changes the equation.

Instead of revealing full identity records, users prove specific attributes. This approach is often referred to as privacy preserving compliance or zero knowledge KYC.

The model works as follows:

- A trusted verifier conducts KYC, AML, and sanctions screening off chain.

- The verification result becomes a credential issued to the user’s wallet.

- When a crypto neobank or DeFi protocol needs confirmation, it receives a zero knowledge proof rather than raw documents.

The institution still enforces compliance rules.

The regulator retains confidence that AML and sanctions policies are applied.

The user keeps control of underlying personal data.

This enables on chain identity verification without putting personally identifiable information on chain. It shifts identity from static, duplicated records to reusable cryptographic credentials.

For crypto neobanks aiming to scale globally, this architectural shift is not optional. It is foundational.

What Zero Knowledge Identity Unlocks for Crypto Neobanks

Once identity becomes reusable and portable, the design space of crypto banking expands significantly.

Under Collateralized Lending and Crypto Credit Cards

Most DeFi lending remains over collateralized because identity is weak. With persistent zkKYC credentials and Sybil resistant identity, crypto neobanks can begin underwriting based on verified risk tiers rather than wallet balances alone.

This creates a path toward under collateralized credit and compliant crypto credit products.

How zkKYC Works: Understanding the Mechanisms Behind Privacy Preserving Verification

Cross Border Accounts and Global Remittances

Global crypto banking products must navigate jurisdiction rules, age requirements, and local compliance thresholds.

With zero knowledge identity, smart contracts can enforce these policies at the protocol level. A user can prove residency, KYC tier, or accreditation status without exposing full documents. This supports cross border payments and remittances while remaining regulator ready.

Enterprise and B2B Financial Flows

Enterprise adoption requires strong compliance infrastructure. CFOs and compliance teams need clear risk segmentation and enforceable access controls.

Zero knowledge credentials allow crypto neobanks to offer enterprise grade compliance without turning every transaction into a permanently exposed identity record. This is essential for payroll, treasury management, and B2B crypto payments.

Together, these use cases define what privacy and compliance parity actually looks like in a Web3 banking environment.

zkMe: Building the Identity Layer for Compliant Crypto Banking

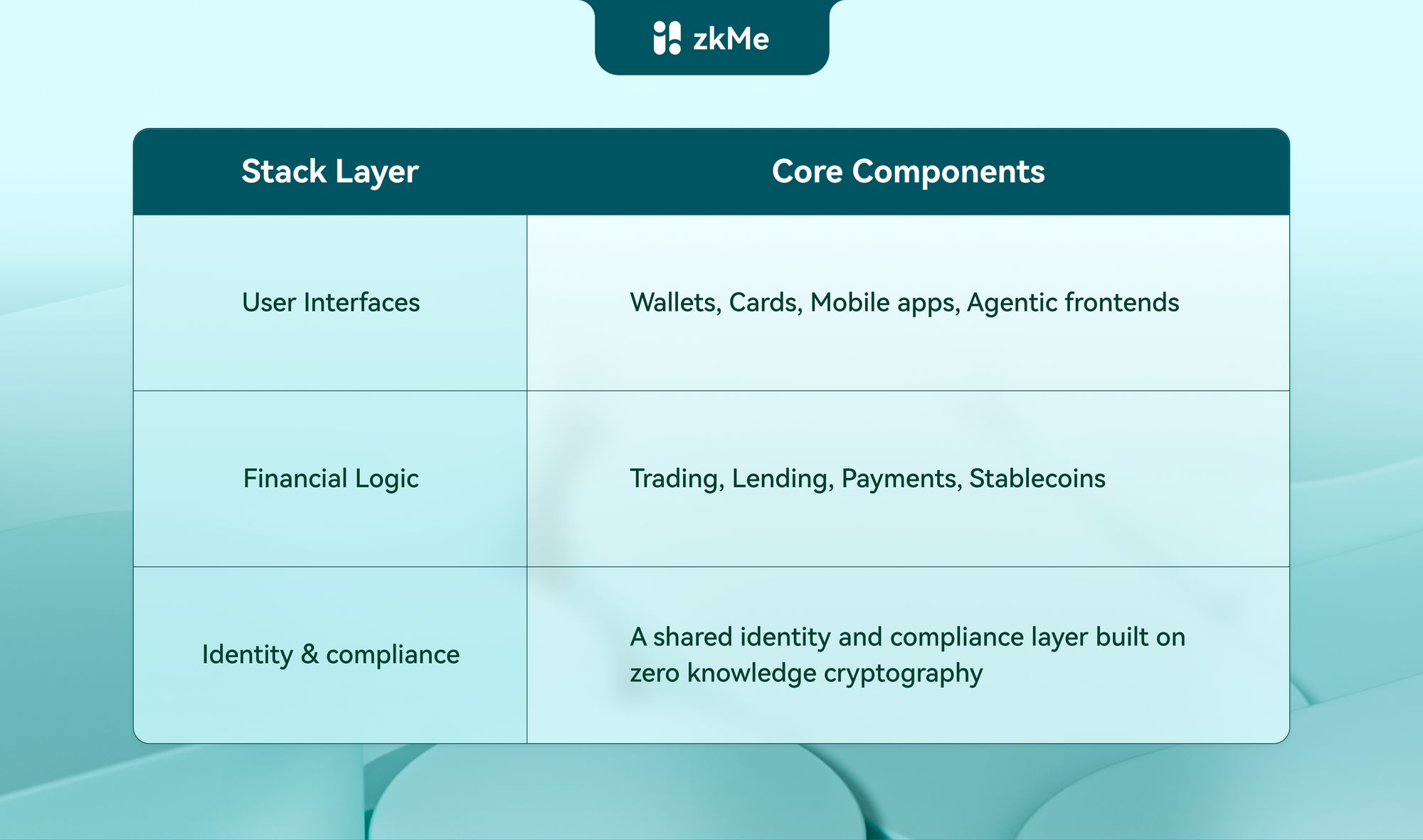

At zkMe, we see permissionless neobanks as a new financial stack composed of three layers:

zkMe is designed to serve as that identity layer.

- We run comprehensive KYC, AML, and risk assessments once.

- We issue reusable zero knowledge credentials that work across chains and applications.

- We allow builders to enforce granular compliance policies without directly handling raw personal data.

This is not about bypassing regulation. It is about modernizing compliance infrastructure for crypto finance.

If this layer is implemented correctly, crypto neobanks no longer face a forced trade between regulatory risk and user surveillance. They can achieve regulatory grade compliance with a strictly stronger privacy model than traditional digital banks.

Ready to build the crypto neobank?

Start with a zk-powered identity layer today!

The Real Challenge for Permissionless Neobanks

The defining question for crypto banking is not "CeFi vs DeFi" or "On-chain vs Off-chain".

The real challenge is whether we can design financial infrastructure where privacy enhancing technology strengthens compliance instead of undermining it.

Permissionless neobanks will only become mainstream when regulators trust them and users prefer them. Achieving both requires rethinking identity at the protocol level.

Zero knowledge identity makes privacy preserving compliance possible.

That is the standard we are building toward at zkMe.

If you are building a crypto neobank, a compliant DeFi protocol, or a global Web3 payment product, and want to explore this architecture, we are always open to comparing notes.

About zkMe

zkMe provides protocols and oracle infrastructure for the compliant, self-sovereign, and private verification of Identity and Asset Credentials.

It is the only decentralized solution capable of performing FATF-compliant CIP, KYC, KYB, and AML checks natively onchain, without compromising the decentralization and privacy ethos of Web3.

By combining zero-knowledge proofs with advanced encryption and cross-chain interoperability, zkMe enables verifiable identity and compliance data to remain entirely under the user's control. This ensures that sensitive information never leaves the user's device while maintaining regulatory-grade assurance for partners and protocols.